|

Site Search and Site Map

Site Search and Site Map

Table of Contents

Money

I. The Functions of Money: Anything that serves

the four functions of money is money.

-

Money serves as

a medium of

exchange, an asset that sellers will accept as payment. A

medium of exchange allows people to eliminate the use of barter.

-

As a unit of accounting,

money is used to measure the value of goods and services relative to

other goods and services ... a way of placing a specific price on economic

goods and services.

-

Money is a store of value or

of purchasing power (the ability of an item to hold value over time).

-

Money serves as a

standard of

deferred payment. That's the property

of an asset that makes it desirable for use as a means of settling debts maturing

in the future.

II. Liquidity: The degree to which an asset

can be acquired or disposed of without much danger of intervening loss in nominal

value and with small transactions costs. Money is the most liquid asset. The opportunity

cost of holding money is the interest yield obtainable by holding some other asset.

III. Monetary Standards, or What Backs Money:

In the US coins, paper currency and balances in transactions accounts are accepted

in exchange for items sold. The payments arise from a fiduciary monetary system.

A fiduciary monetary system is one in which currency is issued by the government,

and its value is based uniquely on the public’s faith that the currency represents

command over goods and services.

-

Acceptability: Transactions accounts and currency

are money because they are accepted on exchange for goods and services. They

are accepted because people have confidence that they can later be exchanged

for other goods and services, since such exchanges have occurred in the past

without problems.

-

Predictability of Value: The purchasing power of

the dollar (that is, its value) varies inversely with the price level. Money

retains its usefulness even if its value declines year in and year out, because

of the predictability of its value in the future.

IV. Defining Money: The money supply is the

amount of money in circulation.

-

The Transactions Approach to Measuring Money:

M1 is the total value of currency plus checkable deposits (demand deposits in commercial

banks and other checking accounts in thrift institutions) and travelers checks

not issued by banks.

-

currency: coins minted by the US Treasury and

paper currency, usually in the form of Federal Reserve notes issued by the

Federal Reserve banks

-

checkable deposits: any deposit in a thrift

institution or a commercial bank on which a check may be written

-

travelers checks: financial instruments purchased

from a non-banking institution that can be used as cash

-

The Liquidity Approach

to Measuring Money: M2:

M2 is M1 plus near monies. (See below.)

-

saving deposits: Interest-earning funds that

can be withdrawn at any time without payment of a penalty but still earn

interest. These include money market deposit accounts that pay a market

interest rate with a minimum balance, limit on transactions and no maturity

date.

-

small-denomination time deposits: Time deposits

are deposits in a financial institution that in principle require a notice

of intent to withdraw or must be left for an agreed period. Withdrawal of

funds prior to the end of the agreed period results in a penalty. Time deposits

include savings certificates and small certificates of deposit (CDs). To

be included in the M2 definition of the money supply, such time deposits

must be less than $100,000. A time deposit has a fixed maturity date and

is offered by banks and other financial institutions.

-

money market mutual fund balances: Deposits

held by investment companies that obtain funds from the public. These funds

are held in common and used to acquire short-term credit instruments, such

as certificates of deposit and securities sold by the US government.

-

M2 and other money supply definitions: Economists

and researchers have come up with even broader definitions of money than

M2. More assets are simply added to the definition. Currently the MZM definition

of money is preferred by some business people and policymakers.

MZM is the

sum of M1 and the deposits in M2 that do not have a set maturity.

Changes in the money supply affect important

economic variables in the short-run.

The

Money Supply: Measuring M1 and M2 from the

Federal Reserve Bank of San Francisco The

Money Supply: Measuring M1 and M2 from the

Federal Reserve Bank of San Francisco

We,

the Economy Films: Chapter 2: What is money? We,

the Economy Films: Chapter 2: What is money?

What is the real value of a dollar? You think that a dollar bill is money

and that banks are where your cash is stored and safeguarded. Well, you’re wrong.

Like, really wrong.

What do banks do with our deposits? Part II about money

What is the Federal Reserve? When the Federal Reserve Chairman awakes

with amnesia only moments before a big press conference, his children, maid

and intern must explain the Fed to him using the only thing handy: the children’s

toys.

What causes a recession? “Recession” mounts an entertaining and educational

look at what causes an economic recession and how recovery is stimulated.

How does Wall Street influence the economy? On the heels of the financial

crisis, Wall Street for some has become synonymous with corruption and greed.

Learn how Wall Street really influences the economy and impacts all of our lives.

Test Yourself: Money

Financial Intermediation and

Banks

I. The US Banking System: The US banking system

is headed by a central bank called the Federal Reserve System. There are a large

number of commercial banks, which are privately owned, profit-seeking institutions.

Other depository institutions are called thrifts or thrift institutions. They consist

of savings and loan associations, mutual savings banks and credit unions.

-

Direct Versus Indirect Finance: Direct finance

occurs when people lend to a business by buying a bond. Indirect finance occurs

when people acquire a liability of a financial intermediary such as a bank,

which lends the funds to a business.

-

Financial Intermediation: The process by which

financial institutions transfer funds from savers to investors.

-

Asymmetric Information, Adverse Selection,

and Moral Hazard: Three reasons why people might wish to direct their funds

through financial intermediaries. The problems arising from asymmetric information,

adverse selection, and moral hazard can be reduced by lending to a financial

institution that will be better able to evaluate the creditworthiness of

business borrowers and monitor their progress until the loans are repaid.

-

Larger Scale and Lower Management Costs: Intermediaries

pool the funds of large numbers of savers, thereby increasing the scale

of the savings managed by an intermediary. Management costs and risks are

lower than they would be if every saver tried to manage his/her lending.

-

Financial Institution Liabilities and Assets:

Financial intermediaries’ liabilities are sources of funds and its assets

are its uses of funds.

-

International Financial Intermediation:

Some countries limit intermediation to within their national boundaries by legal

restraints called capital controls. Other countries have few or no capital controls

that allow for international financial diversification. Often this is through

very large international banks called megabanks.

|

|

|

|

Flow of Funds in the Financial System

Borrowers can borrow funds

directly from lenders in financial markets by selling financial

instruments, such as certificates of deposit, commercial paper,

corporate bonds, government securities and stocks. This method (at

the bottom of the figure) is often called direct finance.

In general, investment banks and brokerage firms play an important

role in helping borrowers raise capital or borrow money using this

method.

The second method for

moving money (at the top of the figure) involves financial

intermediaries that link lenders/savers and borrowers/spenders.

Financial intermediaries fall into three broad categories: (1)

banks and other deposit-taking institutions, (2) life insurance

companies and pension funds and (3) asset management companies.

Typically, banks are financial intermediaries that accept

deposits from individuals and institutions and make loans.

Insurance companies and pension funds take in savings

from households and firms, and invest them in money market

and capital market instruments as well as other assets. Asset

management companies provide professional investment services.

|

The Central Bank and the Banking

System

Private member banks hold

100% of the stocks of the twelve regional federal reserve banks

that make up the Fed. These stocks may not be sold or pledged as

collateral for loans. The member banks receive a 6% dividend annually

on their stock. The remaining 94% goes to the US treasuries, although

they do not hold any stocks.

|

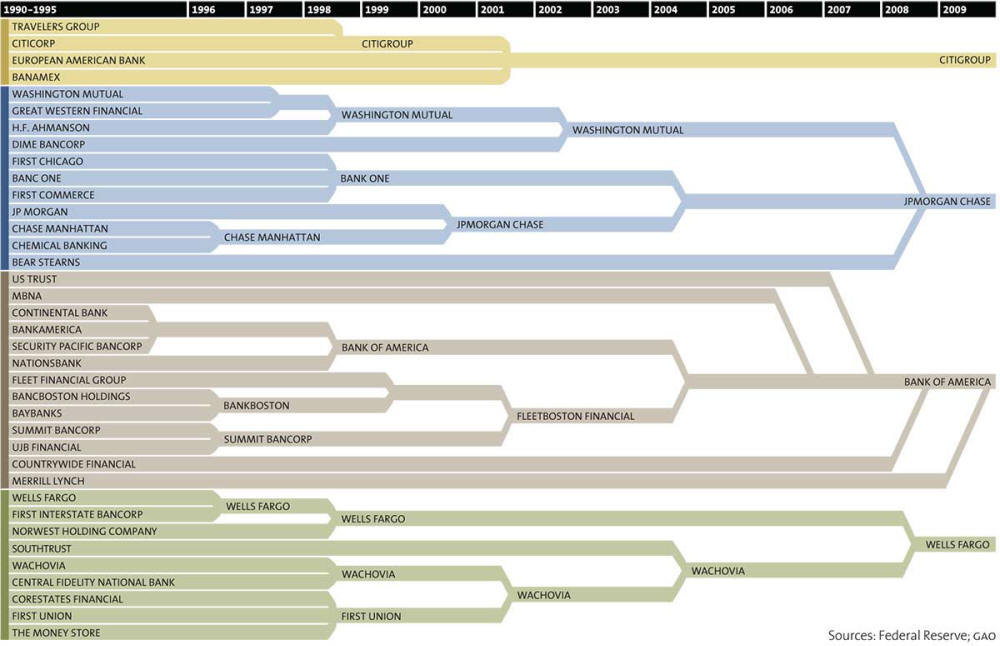

II. Banking Structures Throughout the World:

Multinational businesses have relationships with megabanks based in many nations.

Banking systems vary from banks being a crucial component of the financial intermediation

process to being simply part of a varied financial system. There are also differing

legal environments regulating banks.

-

A World of National Banking Structures: The extent

to which banks are the predominant means by which businesses finance their operations

is one way that national banking systems differ. Another important way is universal

banking in which banks can offer a full range of financial services. Other countries,

including the United States limit universal banking.

-

Central Banks

and Their Roles: The duties of central

banks are in three categories. Central banks perform banking functions for their

governments, provide financial services for private banks, and conduct their

nations’ monetary policies.

III. The Federal Reserve System: The Federal

Reserve System, or the Fed, is the most important regulatory agency in our entire

monetary system and is considered the monetary authority.

-

Organization of the Federal Reserve System: There

are 12 regional Federal Reserve banks each headed by a president. The main authority

of the Fed resides with the Board of Governors of the Federal Reserve System,

whose seven members are appointed for 14-year terms by the president and confirmed

by the Senate. Open-market operations are carried out through the Federal Open

Market Committee (FOMC), consisting of the seven members of the Board of Governors

plus five presidents of the regional banks (always including the president of

the New York bank with the others rotating).

-

Depository Institutions: These are the banks and

other financial institutions that accept deposits that make up our banking system

and consist of approximately 8,000 commercial banks, 1,500 savings and loan

associations, and 12,000 credit unions.

-

Functions of the Federal Reserve System: The Fed

is the nation’s monetary authority.

-

Supplies the Economy with Fiduciary Currency:

The Federal Reserve banks must supply the economy with paper currency called

Federal Reserve notes.

-

Provides a System for Check Collection and

Clearing: The Federal Reserve has established a clearing mechanism for checks

to be deposited in one location and, eventually, clear the account of both

payee and payer.

-

Holds Depository Institutions’ Reserves: The

12 Federal Reserve banks hold the reserves (other than vault cash) of depository

institutions. Depository institutions are required by law to keep a certain

percentage of their deposits in reserves.

-

Acts as the Government’s Fiscal Agent: The

Federal Reserve is the banker and fiscal agent for the federal government.

-

Supervises Depository Institutions: The Fed

along with the Comptroller of the Currency, the Federal Deposit Insurance

Corporation, the Office of Thrift Supervision in the Treasury Department,

and the National Credit Union Administration is a supervisor and regulator

of depository institutions.

-

Acts as a Lender of Last Resort: The Fed stands

ready to bail out any part of the banking system that is in trouble, i.e.,

it will lend money to troubled depository institutions.

-

Regulates the Money Supply: The Fed’s most

important function is its ability to regulate the nation’s money supply.

The major task of the Fed is to manage the supply of money.

-

Intervenes in Foreign Currency Markets: Sometimes

the Fed buys and sells US dollars in foreign exchange markets to keep the

value of the dollar from changing.

IV. Links Between Changes in the Money Supply and

Other Economic Variables: There is a relationship between changes in the money

supply and changes in nominal GDP. There is also a loose, direct relationship between

the rate of growth of the money supply and the rate of inflation.

V. The Origins of Fractional Reserve Banking:

Fractional reserve banking originated with goldsmiths as far back as the 1,000 BC

in Greece. A fractional reserve system of banking is one in which depository institutions

hold reserves that are less than the amount of total deposits.

VI. Depository Institution Reserves: In the

US Federal Reserve System reserves are deposits held by district Federal Reserve

banks for depository institutions, plus depository institutions’ vault cash.

-

Legal Reserves: Reserves that depository institutions

are allowed by law to claim as reserves and consist of deposits held at district

Federal Reserve banks and vault cash.

-

Required Reserves: Legal reserves that a depository

institution must hold with the Fed. The required reserve ratio is the percentage

of total reserves that the Fed requires depository institutions to hold in the

form of vault cash or on deposit with the Fed.

-

Excess Reserves: The difference between legal reserves

and required reserves.

VII. The Fed’s Direct Effect on the Overall Level

of Reserves: A change in the level of reserves causes a multiple change in the

total money supply. The Federal Open Market Committee (FOMC) conducts open

market operations which involves the buying and selling of existing US government

securities in the open private market by the Fed.

VIII. Money Expansion by the Banking System:

The Fed purchases a US government security with a check written on itself from a

bond dealer who deposits the Fed’s check in a bank. Even with fractional reserve

banking, if excess reserves are zero, deposits cannot expand unless total banking

system reserves are increased. The original new deposit was in the form of a check

written on a Federal Reserve district bank. It, therefore, represented new reserves

to the banking system. Only when excess reserves exist or are created by the Federal

Reserve System can the money supply increase.

IX. The Money Multiplier

-

Forces That Reduce the Money Multiplier

-

Leakages: The entire proceeds of a loan

are not always deposited in another bank.

-

Currency Drains: When deposits increase,

the public may want to hold more currency. The greater the amount of

cash leakage, the smaller the deposit expansion multiplier.

-

Excess Reserves: Depository institutions

may wish to maintain excess reserves. Depository institutions do not,

in fact, always keep excess reserves at zero. The greater the excess

reserves, the smaller the deposit expansion multiplier.

-

Real-World Money Multipliers: The maximum

deposit multiplier is never attained for the money supply as a whole because

of currency drains and excess reserves. Each definition of the money supply,

either M1 or M2, will also yield different results for money multipliers.

-

Other Ways in Which the Federal Reserve Can

Change the Money Supply: Engaging in open market operations, a sale of a US

government security by the Fed, results in a decrease in reserves and leads

to a multiple contraction in the money supply. The purchase of a US government

security by the Fed results in an increase of reserves and leads to a multiple

expansion in the money supply.

-

Borrowed Reserves and the Discount Rate:

If a depository institution wants to increase its loans but has no excess

reserves, it can borrow reserves from the Fed. The interest rate that the

Fed charges is called the discount rate.

-

Today’s Discount Rate Policy: Currently

the Fed keeps the discount rate 1 percent above the federal funds interest

rate to discourage borrowing by depository institutions unless they have

severe liquidity problems.

-

Reserve Requirement Changes: The Fed

can alter the money supply by changing reserve requirements.

-

Sweep Accounts and the Decreased Relevance

of Reserve Requirements: A sweep account is a depository institution account

that entails regular shifts of funds from transaction accounts that are subject

to reserve requirements to savings deposits that are exempt from reserve requirements.

-

The Great Reserve Requirement Loophole:

Sweep Accounts: By increasing the use of sweep accounts, banks have significantly

reduced the amount of reserves that banks hold in Federal Reserve banks

and made reserves less important.

-

Implications of Sweep Accounts for Measures

of the Money Supply: M1 has hardly increased since 1993 while M2 has grown

by an average about 5% per year. This is because banks use sweep accounts

instead of transactions accounts to avoid reserve requirements. M1 is no

longer used by the Fed as a measure of the economy’s liquidity. The Fed

uses M2 instead.

Positive

and Negative Multiplier Effects

X. Federal Deposit Insurance: Widespread bank

failures create great hardship for individuals and businesses, which depend on the

safety and security of banks.

-

The Rationale for Deposit Insurance: The FDIC,

FSLIC, NCUSIF AND SAIF were established to mitigate the primary cause of bank

failures-the simultaneous rush of depositors to convert their demand or saving

deposits into currency (bank runs).

-

How Deposit Insurance Causes

Increased Risk Taking by Bank Managers: The low price and rates of deposit insurance that do not reflect

all of the relative risk of different loan portfolios gives managers an incentive

to invest in higher yield, and, therefore, higher risk assets, than they would

if they were no deposit insurance. The FDIC was given regulatory powers to offset

the risk-taking temptations to depository institution managers. The financial industry

was organized so as to protect firms in the industry from competition. Market

discipline on the behavior of financial institutions was replaced by regulatory

discipline.

risk-taking temptations to depository institution managers. The financial industry

was organized so as to protect firms in the industry from competition. Market

discipline on the behavior of financial institutions was replaced by regulatory

discipline.

-

Deposit Insurance, Adverse Selection and Moral

Hazard: Asymmetrical information between two parties causes problems prior to

a transaction and after a transaction has taken place.

-

Adverse Selection in Deposit Insurance: This

problem is caused by asymmetric information before a transaction has taken

place. Individuals who are the most undesirable from the other party’s point

of view are the ones who are most likely to want to engage in a particular

transaction (borrowing). Deposit insurance shields depositors from any adverse

effects of risky decisions making them willing to accept more risk. The

result for the FDIC is larger losses.

-

Moral Hazard in Deposit Insurance and the US

Savings and Loan Debacle: Moral hazard arises because of asymmetric information

after a transaction has taken place. In financial markets lenders face the

hazard that borrowers may engage in activities that are contrary to the

lender’s well being. Insured depositors know they will not suffer losses

and have little incentive to monitor a bank’s investment activities or withdraw

their funds in protest of risky behavior. Higher losses result for the FDIC.

The savings and loan debacle occurred because insured depositors

had no incentive to monitor the performance of S&L managers, and they did

not do so. The S&L managers felt that deposit insurance would allow them

to invest in higher yielding but riskier investments since their depositors

were protected.

Money,

Banking and Monetary Policy (PDF)

The Federal Reserve, Monetary Policy and the Economy (PDF)

What is the Economic Function of a Bank?

How Does the Fed Create Money?

The Federal Reserve Today (PDF) - Use this as a reference for any Fed questions

you may have.

What is the Fed's new policy framework, and why does it matter?

(08/27/02)

Federal

Reserve Board

A Guide to the Fed: Whose Words Carry the Most Weight

What is the Relationship Between the Discount Rate and Mortgage Rates?

Test Yourself: Financial Intermediation and Banks

Monetary Policy

I. What’s So Special About Money? Money is involved

on one side of every non-barter transaction in the economy. Changes in the amount

of money in circulation will have an effect on many transactions and, thus, upon

elements of GDP. Money is a “social contract” in which people agree to express prices

in terms of a common unit, called the dollar in the United States and use as a specific

medium of exchange.

-

Holding Money: Because everyone engages in a flow

of transactions, money must be held in order to buy goods and services. To use

money, one must hold money.

-

The Demand for Money (What People Wish to Hold):

The demand for money can be broken down into three components.

-

transaction demand: Holding money as a

medium of exchange. The level varies directly with nominal national income.

-

precautionary demand: Holding money is

to meet unplanned expenditures and emergencies. The cost is foregone interest

earnings, but this is offset by the security provided.

-

asset demand: Holding money as a store

of value as opposed to having other assets such as small CDs, corporate

bonds and stocks.

-

The Demand for Money Curve: If the amount of money

demanded for transactions is fixed at a certain income level, assuming that

the interest rate represents the cost of holding money, i.e. the opportunity

cost of holding money, the demand for money curve shows a downward slope.

II. The Tools of Monetary Policy:

The Fed uses

several tools in its policy-making efforts to alter consumption, investment

and aggregate demand.

-

Open Market Operations:

The Fed controls the money supply through the purchase and sale of government

securities. The government securities that are used in open market

operations are Treasury bills, bonds and notes. Starting

from an equilibrium level, if the Fed wants to conduct open market operations,

it has to induce individuals, businesses and foreigners to hold more or less

US Treasury securities. The inducement is in the form of making people better off

by causing a change in the price of securities.

-

The Sale of Securities: When the Fed wishes to increase

its sales of government securities, it lowers security prices.

-

The Fed’s Purchase of Securities: When the Fed wishes

to purchase government securities, it raises security prices.

-

The Relationship Between the Price of

Securities and the Rate of Interest: The market price of existing

securities (and all fixed-income

assets) is inversely related to the rate of interest.

Open market operations are the most frequently-used tool of monetary policy

because of their flexibility and immediate effects. Open market operations are

the Fed’s purchases and sales of government

securities with member banks and the

public. When the Fed buys

securities from a bank, it creates reserves in the bank’s

deposit with the Fed, which the bank can then lend to customers. When the Fed

buys

securities from the public, it puts a check in the hand of the consumer, who

can deposit the funds in his bank. The two transactions are slightly different

in effect, because the bank can loan the full excess reserves resulting from

its sale of

securities to the Fed, but the bank must keep the required reserves from

the customer’s deposit, leading to a smaller increase in the money supply. In

either case, the Fed increases the money supply when it buys

securities, and it reduces

the money supply when it sells

securities.

-

Changes in the Difference Between the

Discount Rate and the

Federal Funds Rate: The discount rate is the interest

rate the Fed charges banks when they borrow from the Fed. When it was first

created, the Fed used the discount

rate to carry out monetary policy because it had no power over

reserve requirements and its initial portfolio of government securities was practically

nonexistent. Since 2003 the Fed has kept the discount rate 1 percentage point

above the Federal Funds interest rate.

A reduction in the discount rate encourages banks to borrow from the Fed and,

in turn, increase loans to their customers. As a result, the money supply increases.

An increase in the discount rate discourages banks from borrowing from the Fed,

reducing loans and the money supply.

-

Changes in Reserve Requirements: The Fed

decreased reserve requirements on checkable deposits to 10% in 1992. If the

Fed increases reserve requirements banks reduce their lending by raising interest

rates. If the Fed decreases reserve requirements, banks increase their lending

of their excess reserves by reducing interest rates.

The reserve requirement is the most powerful tool of monetary policy, so it

is only rarely used. A change in the percentage of deposits the banks must hold

in reserve directly impacts the bank’s ability to increase loans and, therefore,

the money multiplier. If the Fed increases the reserve requirement, banks cannot

loan as much and the money supply falls. A reduction in the reserve requirement

increases the potential growth of the money supply.

-

Term auction facilities

were added as a fourth tool of monetary policy

during the Great Recession starting in 2007. Banks secretly bid to borrow money

from the Fed, similar to the function of discount rates, but the secrecy helped

to shield the banks from customer concerns about the banks’ solvency. It is

believed that this tool will primarily be used in times of economic crisis.

III. Effects of an Increase in the Money Supply:

If a large sum of money were arbitrarily distributed to people, they would have

too much money relative to other things that they owned. There are a variety of

ways to dispose of this “new” money.

-

Direct Effect: Excess money would cause aggregate

demand to rise, because an increase in the money supply at any given price level

would cause people to want to purchase more output of real goods and services.

-

Indirect Effect: When there is excess money some

people would deposit it in banks. The recipient banks would have higher reserves

than necessary and would lower interest rates to induce people to borrow. The

increased loans would create a rise in aggregate demand.

-

The Effects of Expansionary Monetary Policy: The

direct and indirect effects of an expansionary monetary policy are to increase

aggregate demand, real GDP, and the price level.

-

The Effects of Contractionary Monetary Policy:

The direct and indirect effects of a contractionary monetary policy are to decrease

aggregate demand, real GDP, and the price level.

IV. Open-Economy Transmission of Monetary Policy:

In an open economy, international trade and purchase/sale of all assets and currencies

must be considered.

-

The Net Export Effect: Expansionary monetary policy

will cause interest rates to fall. Foreigners will demand fewer dollars for

financial assets in the United States and the dollar will depreciate. The net

export effect of expansionary monetary policy will be positive because exports

will increase and imports will decrease.

-

Contractionary Monetary Policy: Contractionary

monetary policy will cause interest rates to rise, thus, financial capital will

flow into the United States. The demand for dollars will increase and the dollar

will appreciate. The result will be an increase in imports and a decrease in

exports.

-

Globalization of International Money Markets: If

the Fed reduces the growth of the money supply, individuals and firms in the

United States can increasingly obtain dollars from other sources. Due to the

increase in technology, money transactions, on a global scale, can take place

at the push of a button.

V. Monetary Policy and Inflation: Studies show

a relatively stable relationship between excessive growth in the money supply in

circulation and inflation in the long run. If the supply of money rises relative

to the demand for money, it takes more units of money to purchase goods and services.

-

The Equation of Exchange and the Quantity Theory:

The equation of exchange says that the number of monetary units (M) times the

number of times each unit is spent on final goods and services (V) is identical

to the price level (P) times real GDP (Q) or MV = PQ. This equation shows the

relationship between changes in the quantity of money in circulation and the

price level.

-

The Crude Quantity Theory of Money and Prices:

By making assumptions about variables in the equation of exchange a simplified

theory, the quantity theory of money and prices, can be derived, to explain

why prices change. The results reveal that a proportionate change in the money

supply leads to a proportionate change in the price level.

-

Empirical Verification: There is considerable evidence

for the validity between excessive monetary growth and high rates of inflation.

Inflation can be a result of expansionary

monetary policy if the economy is too robust and creates too much money. Many

people incorrectly believe that inflation comes from high prices. In fact, inflation

occurs when there is so much money chasing available goods and services that

the money loses its value in relation to the products it purchases. This results

in higher prices for the limited products because buyers are in effect competing

to buy them and the highest price paid wins. Expansionary monetary policy also

restricts deflation, which occurs during recessions when there is a shortage

of money in circulation and companies lower their prices in order to attract

business. This also results in higher unemployment and reduced wages.

VI. Monetary Policy in Action: The Transmission

Mechanism

-

The Keynesian Transmission Mechanism: This theory

asserts that the main effect of monetary policy is through changes in the interest

rate. Money supply changes cause changes in the interest rate. That changes

planned investment and that causes changes in income and employment.

-

The Monetarist’s Transmission Mechanism:

Monetarists

believe that changes in the money supply lead to changes in nominal GDP in the

same direction. An increase in money supply leads the public to have larger

holdings than desired, which induces them to buy more of every-thing. Ultimately,

the public simply bids up prices so the price level rises.

-

Monetarists’ Criticism of Monetary Policy: Monetarists

see monetary policy as a destabilizing force in the economy. They believe policy

makers should follow a monetary rule; increase the money supply smoothly at

a rate consistent with the economy’s long-run average growth rate. A monetary

rule is a monetary policy that incorporates a rule specifying the annual

growth rate of some monetary aggregate.

VII. Fed Target Choice: Interest Rates or Money

Supply? Money supply and interest rate targets cannot be pursued simultaneously.

Interest rate targets force the Fed to abandon control over the money supply. Money

stock growth targets force the Fed to allow interest rates to fluctuate.

VIII. The Way Fed Policy is Currently Implemented:

The Fed announces interest rate targets. If it says it is lowering the interest

rate, it means that it is engaging in expansionary monetary policy. If it says it

is increasing the interest rate, it means that it is engaging in contractionary

monetary policy.

Low

interest rates paid by banks on their CDs and savings accounts and low interest

rates available in bonds make saving money less attractive because the interest

earned is minimal. When prices on goods and services start to rise as the economy

expands, consumers and businesses find that saving money at 5% does not keep

up with price increases of 10% or more at the grocery store and business suppliers.

Expansionary monetary policy works because people and businesses tend to seek

better returns by spending their money on equipment, new homes, new cars, investing

in local businesses and other expenditures that promote the movement of money

throughout the system, increasing economic activity.

A

liquidity trap is a situation, described in Keynesian economics, in which

injections of cash into the private banking system by a central bank fail to

decrease interest rates and hence make monetary policy ineffective. Central

banks may lower interest rates right down to the zero-bound level but the economy

may still fail to respond. A liquidity trap occurs when people hoard cash because

they expect an adverse event such as deflation, insufficient aggregate demand

or war. Common characteristics of a liquidity trap are interest rates that are

close to zero and fluctuations in the money supply that fail to translate into

fluctuations in price levels. In a liquidity trap, bonds pay little or no interest,

which makes them nearly equivalent to cash. Under the narrow version of Keynesian

theory in which this arises, it is specified that monetary policy affects the

economy only through its effect on interest rates. Thus, if an economy enters

a liquidity trap, further increases in the money stock will fail to further

lower interest rates and, therefore, fail to stimulate the economy.

How

Monetary Policy Works (covers several screens using the Next links

at the bottom of each)

Monetary Policy: Stabilizing Prices and Output

A Look at Fiscal and Monetary Policy

(sometimes slow to load)

Monetary

Policy Roles and Responsibilities

Pros and Cons of Contractionary Monetary Policy

IX. Active vs. Passive Policymaking

Active (discretionary) policymaking is all actions

on the part of monetary and fiscal policymakers that are undertaken in response

to or in anticipation of some change in the economy. Passive (nondiscretionary)

policymaking is policy based on a rule such as the monetarists’ monetary rule.

X. The Natural Rate of Unemployment:

The rate of unemployment that is estimated to prevail in long-run macroeconomic

equilibrium when all workers and employers have fully adjusted to any changes in

the economy. The rate consists of two parts: (1) frictional unemployment, which

exists due to individuals taking time to search for the best job opportunities and

(2) structural unemployment due to rigidities in the economic system. These rigidities

include union activity that sets wages above equilibrium and restricts the mobility

of labor, licensing arrangements that restrict entry into specific professions,

minimum wage laws and other laws that require all workers to be paid union wage

rates on government contract jobs, welfare and unemployment insurance that reduces

incentives to work and a mismatch of skills with available jobs.

-

Departures From the Natural Rate of Unemployment:

Deviations of the actual unemployment rate from the natural rate are due to

cyclical unemployment. This results from business recessions that occur when

aggregate demand is insufficient to create full employment.

-

The Impact of Expansionary Policy: Unanticipated

fiscal or monetary policy to stimulate the economy causes the price level

and real output to rise.

-

The Consequences of Contractionary Policy:

An unanticipated reduction in aggregate demand results in a fall in the

price level and real GDP.

-

The Phillips Curve: A Rationale for Active Policymaking?

A curve showing the relationship between the unemployment rate and changes in

wages or prices. It was long thought that the Phillips curve depicted a trade-off

between unemployment and inflation. If there is an unexpected increase in aggregate

demand, greater inflation and lower unemployment will result. An unexpected

decrease in aggregate demand results in greater deflation and higher unemployment.

-

The Negative Relationship Between Inflation

and Unemployment: Looking at both increases and decreases in aggregate demand,

it is clear that high inflation rates are associated with low unemployment

and low inflation with high unemployment.

-

Is There a Trade-Off? The negative relation

between the inflation rate and the unemployment rate has come to be called

the Phillips curve. Policymakers thought that decreases in the unemployment

rate through expansionary fiscal policy would result in a higher rate of

inflation. It turned out to not be that simple.

-

The NAIRU: The NAIRU is a non-accelerating

inflation rate of unemployment which is the rate of unemployment below which

the rate of inflation tends to rise and above which the rate of inflation

tends to fall.

-

The Importance of Expectations: If wage offers

to unemployed workers are unexpectedly high, these workers believe that the

higher nominal wages are increases in real wages if aggregate demand fluctuates

at random. But, if policy makers attempt to exploit the trade-off in the Phillips

curve, aggregate demand will no longer fluctuate in a random manner.

-

The Effects of Unanticipated Policy: If the

Fed attempts to reduce the unemployment rate, it must increase the money

supply enough to produce a certain inflation rate.

-

Adjusting Expectations and a Shifting Phillips

Curve: Once workers expect the higher inflation rate, the rising nominal

wage will no longer be sufficient to entice them out of unemployment and

the unemployment rate will rise. If authorities continue the stimulus to

keep unemployment down, worker’s expectations will adjust. Thus, policymakers

cannot choose a permanently lower unemployment rate and in the long run

have an unchanged unemployment rate at the expense of a permanently higher

inflation rate.

XI.

The Rational Expectations and the Policy

Irrelevance Proposition: Rational expectations is a theory that states that

people combine the effects of past policy changes on important economic variables

with their own judgment about the future effects of current and future policy changes.

The new classical model is a model in which wages and prices are flexible,

there is pure competition in all markets, and the rational expectations hypothesis

is assumed to be working.

-

Flexible Wages and Prices, Rational Expectations,

and Policy Irrelevance: An increase in the money supply can raise output and

lower unemployment in the short-run, but it has no effect on either in the long

run.

-

The Response to Anticipated Policy: If workers

know an increase in the money supply is about to take place and they know

when it is going to occur, and then they will insist on nominal wages that

move upward with the higher prices.

-

The Policy Irrelevance Proposition: The idea

that a fully anticipated monetary policy is irrelevant in determining the

levels of real variables in either the short run or long run and that even

an unanticipated one has no effect in the long run. When the money supply

changes in an anticipated way the short run aggregate supply curve shifts

to reflect the change. For example, the SRAS will shift upward simultaneously

with an anticipated increase in aggregate demand. The only effect of an

increase in money supply is a rise in price level.

-

What Must People Know? Economic participants

do not have to have perfect information. Even if they are not perfect at

forecasting the future, they are likely to know a lot. The policy irrelevance

proposition really assumes only that people do not consistently make the

same mistakes in forecasting the future.

-

What Happens If People Don’t Know Everything?

Monetary policy can have an effect on real variables in the short-run only

if the policy is unsystematic and unanticipated or if people make forecasting

errors. In the long run this effect will disappear because people will figure

out what is going on and revise their expectations.

-

The Policy Dilemma: The New Classical model suggests

that only “mistakes” can have real effects. If the Fed always does what it intends

and its actions are always correctly anticipated, monetary policy will affect

only price level and nominal input prices. If so, the Fed is effectively precluded

from utilizing monetary policy to lower unemployment or raise the level of real

GDP.

XII. Another Challenge to Policy Activism:

Real Business Cycles: An extension of the theories of the new classical economists

in which money is neutral and only real supply-side factors matter in influencing

labor employment and real output.

-

The Distinction Between Real and Monetary Shocks:

Real business cycle theorists argue that real forces help explain economic fluctuations.

A real shock affects long run and short-run aggregate supply, not aggregate

demand.

-

The Impact on the Labor Market: A rise in the price

level due to a real shock pushes the real wage rate downward and firms reduce

the amount of labor inputs they are using. The real wage rate falls and the

level of employment declines. In the long run, some workers willing to continue

to work at lower wages in the short run, will retire, work part-time, or drop

out of the labor force. The SRAS curve will decrease which puts additional upward

pressure on the price level and downward pressure on real GDP.

-

Generalizing the Theory: Real business cycle theory

examines real disturbances such as technological change and shifts in the composition

of the labor force.

A Comparison Chart

| |

Fiscal Policy

|

Monetary Policy

|

|

Definition

|

Fiscal policy is the use of government expenditure and revenue collection

to influence the economy.

|

Monetary policy is the process by which the monetary authority of a

country controls the supply of money, often targeting a rate of interest

to attain a set of objectives oriented towards the growth and stability

of the economy.

|

|

Principle

|

Manipulating the level of aggregate demand in the economy to achieve

economic objectives of price stability, full employment and economic

growth.

|

Manipulating the supply of money to influence outcomes like economic

growth, inflation, exchange rates with other currencies and unemployment.

|

|

Policy-maker

|

Government (e.g. US Congress, Treasury Secretary)

|

Central Bank (e.g. US Federal Reserve or European Central Bank)

|

|

Policy Tools

|

Taxes, amount of government spending

|

Interest rates, reserve requirements, currency peg, discount window,

quantitative easing, open market operations, signaling

|

Economists

and politicians have argued that monetary policy and fiscal policy are skewed in

an undesirable direction; fiscal deficits are too high and reduce national saving,

while monetary policy produces interest rates that retard investments. It is customary

in a modern economy to separate monetary and fiscal functions. A country’s central

bank determines the monetary policy (interest rates) and the fiscal policy (taxes

and spending) is determined by the executive and legislative branches. But the monetary

and fiscal authorities have different objectives. The central bank takes a stance

that emphasizes austerity and low inflation. The fiscal authorities worry about

full employment, popularity, keeping taxes low, preserving spending programs and

getting re-elected. So they choose high deficits. The central bank wants to minimize

inflation and so chooses high interest rates. The outcome is a non-cooperative equilibrium

between fiscal authorities and monetary policy makers that usually leads to moderate

unemployment, moderate inflation and a low level of investment. Perhaps the best

strategy is to lower the deficits, lower interest rates and raise investment, a

strategy adopted by President Bill Clinton.

A

Topological Mapping of Explanations and Policy Solutions to our Weak Economy

Test Yourself: Monetary Policy

|